Постинг

31.05.2016 11:17 -

Russian central bank says recession's end in sight

Автор: goro82

Категория: Бизнес

Прочетен: 671 Коментари: 2 Гласове:

Последна промяна: 31.05.2016 11:21

Прочетен: 671 Коментари: 2 Гласове:

0

Последна промяна: 31.05.2016 11:21

гр. ДЕВИН-КАВУРСКО КАЛЕ-КЕМЕРОВ МОСТ-РЕЗ...

ВЕКЪТ НА ЛЪВА. КНИГА I, "МИШОКА&quo...

МИШОКА -- 04. Доко II (1)

ВЕКЪТ НА ЛЪВА. КНИГА I, "МИШОКА&quo...

МИШОКА -- 04. Доко II (1)

Russian central bank points to decreasing inflation, rosy summer outlook

Analysts wary of further rouble strength, particularly absent oil price gains

Manufacturing hailed as a success but also remains internationally uncompetitive

The regular paper on economic trends just published by the Russian central bank gives a seasonally sunny outlook for the Russian economy. Inflation is going down, the economy might be finally turning the corner, and there is much budget spending to look forward to in the second half of the year.

The outlook, however, comes with a few contradictions and should be taken with a pinch of salt.

Russian inflation might be trending down and is on target to hit 6.5% (year-over-year) by the end of 2016 and 4% (y/y) by end 2017, according to the report. The problem, however, is that the absolute level of inflation has been stuck above 7% (y/y) throughout the last three months.

The bank expects that consumer price inflation will stay at 7.3% (y/y) at the end of May. The report says that food prices have stopped falling, producer prices are actually on the rise, and the stronger rouble has so far failed to have too much of an impact.

The central bank also points to a massive budget deficit in the second half of the year (at least 4% of GDP, according to the report), which presumably would be partially financed by printing roubles. The deficit hit 8.6% of GDP in April (that must have included a rise in defence expenses, which the report mentions).

All of these things will make it harder for the central bank to hit its year-end inflation targets.

In the longer term, the bank reminds us that unemployment in April went down to 5.9% (from 6% in March). It is presently not too far from its non-inflationary level (non-accelerating inflation rate of unemployment) of 5.5%. There is also not much of an output gap (available spare capacity) in the economy, states the central bank.

This means that economic growth will lead to higher inflation. Real wages were on the rise (y/y) in February and March, but they went down again in real terms in April. It would not be too surprising if the central bank had a hand in this.

The central bank must have a significant degree of input in government discussions on the level of wages in the state sector, which dominates the Russian economy. In the report, the central bank argues that wages in the state sector rose too quickly in 2011-2014 and the current policy of holding them back is reasonable. Importantly, it also helps to keep inflation in check.

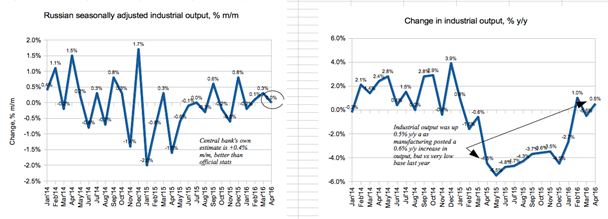

Here, however, lies a major problem and a logical quandary. In the same report, the bank's analysts appear very excited about the growth in industrial output seen in April, which was driven by manufacturing sector. They point to signs of revival in sectors that produce for the domestic market.

They also argue that the official statistics on Russia's industrial output might actually under-estimate the level of industrial recovery in April.

цитирайAnalysts wary of further rouble strength, particularly absent oil price gains

Manufacturing hailed as a success but also remains internationally uncompetitive

The regular paper on economic trends just published by the Russian central bank gives a seasonally sunny outlook for the Russian economy. Inflation is going down, the economy might be finally turning the corner, and there is much budget spending to look forward to in the second half of the year.

The outlook, however, comes with a few contradictions and should be taken with a pinch of salt.

Russian inflation might be trending down and is on target to hit 6.5% (year-over-year) by the end of 2016 and 4% (y/y) by end 2017, according to the report. The problem, however, is that the absolute level of inflation has been stuck above 7% (y/y) throughout the last three months.

The bank expects that consumer price inflation will stay at 7.3% (y/y) at the end of May. The report says that food prices have stopped falling, producer prices are actually on the rise, and the stronger rouble has so far failed to have too much of an impact.

The central bank also points to a massive budget deficit in the second half of the year (at least 4% of GDP, according to the report), which presumably would be partially financed by printing roubles. The deficit hit 8.6% of GDP in April (that must have included a rise in defence expenses, which the report mentions).

All of these things will make it harder for the central bank to hit its year-end inflation targets.

In the longer term, the bank reminds us that unemployment in April went down to 5.9% (from 6% in March). It is presently not too far from its non-inflationary level (non-accelerating inflation rate of unemployment) of 5.5%. There is also not much of an output gap (available spare capacity) in the economy, states the central bank.

This means that economic growth will lead to higher inflation. Real wages were on the rise (y/y) in February and March, but they went down again in real terms in April. It would not be too surprising if the central bank had a hand in this.

The central bank must have a significant degree of input in government discussions on the level of wages in the state sector, which dominates the Russian economy. In the report, the central bank argues that wages in the state sector rose too quickly in 2011-2014 and the current policy of holding them back is reasonable. Importantly, it also helps to keep inflation in check.

Here, however, lies a major problem and a logical quandary. In the same report, the bank's analysts appear very excited about the growth in industrial output seen in April, which was driven by manufacturing sector. They point to signs of revival in sectors that produce for the domestic market.

They also argue that the official statistics on Russia's industrial output might actually under-estimate the level of industrial recovery in April.

This upbeat view on manufacturing seems to be the basis for an economic upgrade by the central bank for the Russian economy. The bank now expects a steady quarter-on-quarter recovery of GDP for the rest of the year. GDP is forecast to increase by 0.1-0.2% (quarter-over-quarter) in the second quarter of 2016, by 0.3% (q/q) in Q3 and by 0.5% (q/q) in Q4.

Russia's GDP was down 0.1% (q/q) in Q1 and 3.7% (y/y) in 2015.

Elsewhere in the report, however, the bank acknowledges that there is no turnaround in investment. Investment, in fact, will continue to contract unless domestic demand (and investments in domestically oriented sectors) rebounds. The central bank analysts believe that Russian export industries are just not competitive internationally (even with a much weaker rouble) and there are very few pockets of investment growth among exporters.

It is hard to reconcile the bank's optimistic view on domestically fuelled economic growth with a belief in restraints on real wages (and therefore subdued domestic demand and investment). And if inflation is a structural problem (the output gap being too narrow, the budget deficit too wide), does it make sense to target wages to keep it under control?

At least, bank's analysts are quite frank and consistent with their view on the rouble. They believe that “the rouble strength could prove to be precarious without further increases in the oil price and with the continuous capital outflows”. This makes more sense, given the downside risks to the oil price.

Capital flight in April was $5.8 billion as Russian banks continued to pay down their FX debts. The outflows could accelerate if the US Federal Reserve hikes rates, according to the report.

This could mean that the Russian central bank has to keep its rates at elevated levels for longer so as to keep the rouble steady and inflation under control.

It just does not, however, quite square up with an imminent economic recovery.

цитирайRussia's GDP was down 0.1% (q/q) in Q1 and 3.7% (y/y) in 2015.

Elsewhere in the report, however, the bank acknowledges that there is no turnaround in investment. Investment, in fact, will continue to contract unless domestic demand (and investments in domestically oriented sectors) rebounds. The central bank analysts believe that Russian export industries are just not competitive internationally (even with a much weaker rouble) and there are very few pockets of investment growth among exporters.

It is hard to reconcile the bank's optimistic view on domestically fuelled economic growth with a belief in restraints on real wages (and therefore subdued domestic demand and investment). And if inflation is a structural problem (the output gap being too narrow, the budget deficit too wide), does it make sense to target wages to keep it under control?

At least, bank's analysts are quite frank and consistent with their view on the rouble. They believe that “the rouble strength could prove to be precarious without further increases in the oil price and with the continuous capital outflows”. This makes more sense, given the downside risks to the oil price.

Capital flight in April was $5.8 billion as Russian banks continued to pay down their FX debts. The outflows could accelerate if the US Federal Reserve hikes rates, according to the report.

This could mean that the Russian central bank has to keep its rates at elevated levels for longer so as to keep the rouble steady and inflation under control.

It just does not, however, quite square up with an imminent economic recovery.